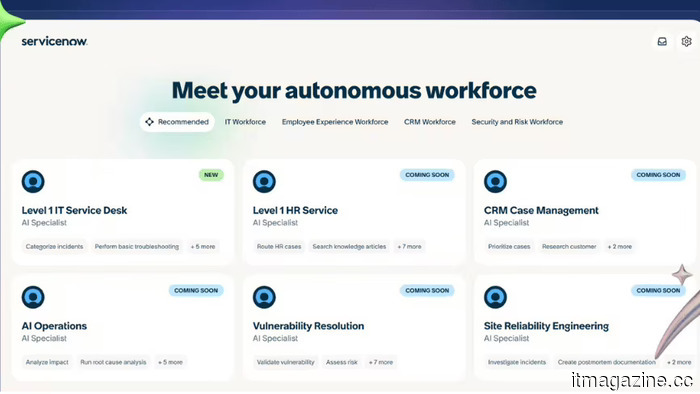

ServiceNow estimates that by 2030, it will reach $30 billion, with one-third of its annual contract value coming from AI.

**TL;DR** On May 4, 2026, ServiceNow utilized its investor day to forecast $30 billion in subscription revenue by 2030, with approximately 30% of that annual contract value (ACV) attributed to Now Assist. This messaging is a strategic response to fears of AI-SaaS displacement.

By 2026, ServiceNow has emerged as a closely monitored case study regarding whether enterprise software firms can adapt to the AI revolution or risk being sidelined. During the investor day, the company provided its most convincing argument to date, with Bloomberg reporting on the forecast of $30 billion in subscription revenue by 2030. Chief Financial Officer Gina Mastantuono indicated that Now Assist, the company's leading AI product, will account for roughly 30% of this anticipated ACV.

The way the investor day was framed was intentional. Coverage from The Cerbat Gem referred to the day’s narrative as a “Control Tower” theme: positioning ServiceNow as the central platform for coordinating, governing, and implementing enterprise AI rather than a vendor whose workflow software might be supplanted by general-purpose models. Mastantuono raised the AI ACV target for the near term from $1 billion to $1.5 billion, with the current Now Assist ACV at about $750 million as of the first quarter of 2026, an increase from $600 million at the close of 2025.

**Why the Pitch Matters Now**

The argument ServiceNow has needed to present throughout 2026 is foundational. Fortune highlighted in April that ServiceNow's robust earnings alone did not quell the wider concerns regarding AI agents and direct model implementations potentially undermining workflow-software middleware, the area where ServiceNow has traditionally operated. Coverage from TNW regarding the new Anthropic enterprise services firm and the finalization of OpenAI's Deployment Company coincided with the ServiceNow announcement and exemplifies the kind of competitive developments that fuel these worries. Both AI-native solutions are now strategically targeting the customer base ServiceNow has cultivated over the last two decades.

ServiceNow's assertion is that it acts as the operating system for enterprise AI deployments rather than being a mere deployment entity. The Now Assist service is positioned as the orchestration layer, with the growth in ACV serving as evidence of customer willingness to invest in that role, and the $30 billion target for 2030 consolidating those claims into a believable long-term revenue projection.

**The Numbers in Context**

ServiceNow anticipates its 2026 subscription revenue to exceed its previous goal of $15 billion by approximately $500 million. The trajectory from that point to over $30 billion by 2030 suggests a sustained growth rate of around 19% annually, which surpasses the industry consensus for legacy SaaS but is below the company’s recent quarterly growth figures. The optimistic scenario presented by the CFO, envisioning $32 billion by 2030, requires Now Assist not only to grow in dollar terms but also to increase its share of total ACV, ultimately reaching about a third of all subscription revenue.

Achieving this goal depends on several factors that public-market investors may view with skepticism. TNW has been monitoring the broader AI multiple-compression trend throughout the spring, with Palantir’s decline and Citi’s price-target reductions serving as the most prominent indicators. ServiceNow's stocks have also been affected by these trends. The projections made during the investor day serve, in part, as a rebuttal: asserting that the company possesses both the customer base and momentum in AI products to substantiate a valuation trajectory that differs from the current pricing of the wider AI-SaaS sector.

**Signals to Watch**

There are three key factors that will determine whether the $30 billion forecast materializes. Firstly, the quarterly ACV progress of Now Assist: achieving growth from $600 million at the end of 2025 to $750 million in Q1, and then to $1.5 billion by year-end, necessitates a level of compounding growth that typically does not occur randomly in enterprise software. Secondly, competitive dynamics will play a role: how many enterprise clients prefer to have their AI deployments orchestrated by ServiceNow rather than by competitors like Anthropic-Blackstone or OpenAI's DeployCo. Lastly, the impact on margins is crucial: so far, ServiceNow’s AI products have mirrored the company-average gross margin; maintaining that as computing costs rise will be key to whether the $30 billion figure generates the necessary cash flows to support the anticipated valuation.

These inquiries cannot be addressed by an investor-day presentation slide. However, they represent the pertinent questions, and ServiceNow appears ready to be evaluated against them. In 2026, that alone serves as a strong competitive indication.

Other articles

Intel has appointed Qualcomm veteran Alex Katouzian to head a new Client Computing and Physical AI division.

Intel has brought on Alex Katouzian, who spent 25 years at Qualcomm, to head a newly formed Client Computing and Physical AI division. This marks the second high-profile recruitment from Qualcomm during CEO Lip-Bu Tan's leadership.

Intel has appointed Qualcomm veteran Alex Katouzian to head a new Client Computing and Physical AI division.

Intel has brought on Alex Katouzian, who spent 25 years at Qualcomm, to head a newly formed Client Computing and Physical AI division. This marks the second high-profile recruitment from Qualcomm during CEO Lip-Bu Tan's leadership.

Intel has recruited Qualcomm veteran Alex Katouzian to head a newly formed group focused on Client Computing and Physical AI.

Intel has brought on Alex Katouzian, who spent 25 years at Qualcomm, to head a newly formed group that combines Client Computing and Physical AI. This marks the second senior recruitment from Qualcomm during CEO Lip-Bu Tan's time in office.

Intel has recruited Qualcomm veteran Alex Katouzian to head a newly formed group focused on Client Computing and Physical AI.

Intel has brought on Alex Katouzian, who spent 25 years at Qualcomm, to head a newly formed group that combines Client Computing and Physical AI. This marks the second senior recruitment from Qualcomm during CEO Lip-Bu Tan's time in office.

Metalenz's latest face scan technology is integrated beneath the phone display, eliminating the need for unsightly cutouts.

Metalenz has just demonstrated that payment-grade facial recognition can function with a fully lit display, a feat that Apple has been attempting to achieve for years without success.

Metalenz's latest face scan technology is integrated beneath the phone display, eliminating the need for unsightly cutouts.

Metalenz has just demonstrated that payment-grade facial recognition can function with a fully lit display, a feat that Apple has been attempting to achieve for years without success.

Next-generation DDR6 memory, boasting incredible speeds, is currently in development, but it will be a considerable wait.

Samsung, SK Hynix, and Micron have initiated early development of DDR6 in collaboration with substrate manufacturers, aiming for speeds that surpass DDR5 by more than two times, although mass production remains years in the future.

Next-generation DDR6 memory, boasting incredible speeds, is currently in development, but it will be a considerable wait.

Samsung, SK Hynix, and Micron have initiated early development of DDR6 in collaboration with substrate manufacturers, aiming for speeds that surpass DDR5 by more than two times, although mass production remains years in the future.

Nscale has invested €695 million in Portugal, while Microsoft contributes to a crypto-to-AI neocloud that has reached a valuation of $14.6 billion in just two years.

Nscale is set to provide 66,000 Nvidia Rubin GPUs to Microsoft's 1.2 GW Sines campus. The company, which transitioned from crypto mining, is now the most valuable AI infrastructure startup in Europe, boasting a valuation of $14.6 billion.

Nscale has invested €695 million in Portugal, while Microsoft contributes to a crypto-to-AI neocloud that has reached a valuation of $14.6 billion in just two years.

Nscale is set to provide 66,000 Nvidia Rubin GPUs to Microsoft's 1.2 GW Sines campus. The company, which transitioned from crypto mining, is now the most valuable AI infrastructure startup in Europe, boasting a valuation of $14.6 billion.

Google, Microsoft, and xAI have consented to share governmental evaluations of AI models before their release as the Mythos crisis prompts an increase in oversight.

Five leading AI laboratories are now presenting their models for evaluation by the US government. This voluntary program lacks legal authority but includes all significant AI developers following the Mythos crisis.

Google, Microsoft, and xAI have consented to share governmental evaluations of AI models before their release as the Mythos crisis prompts an increase in oversight.

Five leading AI laboratories are now presenting their models for evaluation by the US government. This voluntary program lacks legal authority but includes all significant AI developers following the Mythos crisis.

ServiceNow estimates that by 2030, it will reach $30 billion, with one-third of its annual contract value coming from AI.

ServiceNow anticipates $30 billion in subscription revenue by 2030, with 30% of that annual contract value (ACV) coming from Now Assist, the company's premier AI product. The presentation during the investor day addresses concerns regarding potential displacement by AI-SaaS.