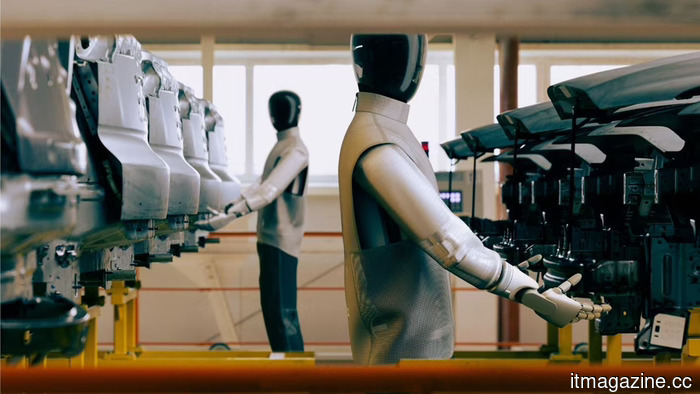

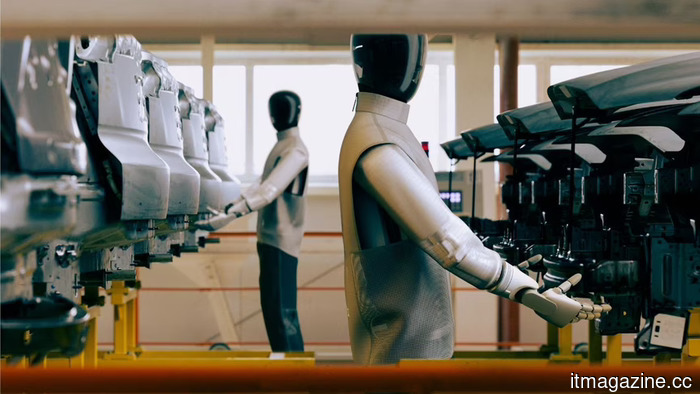

Barclays reports that humanoid robots could help alleviate 60% of the anticipated 37 million worker shortage in China by 2035.

The recent note from the British bank predicts that humanoid robots could alleviate 60% of the anticipated decline in the labor force by 2035, as China's workforce is projected to decrease by 37 million people in the next decade. This would necessitate the deployment of up to 24 million humanoid robots.

Barclays' research estimates that China's implementation of humanoid robots could counteract as much as 60% of the expected decline in its labor force by 2035.

The calculations underpinning this estimate reveal its significance. According to Barclays' demographic projections, and assuming a 65% participation rate, China's working-age population is expected to decrease by 37 million in the upcoming ten years.

Manufacturing constitutes about a quarter of China's economy, so a decline of 37 million workers is framed by the bank as an immediate industrial risk rather than a slow demographic issue.

The latest insights from the EU tech arena, a narrative from the experienced founder Boris, along with some dubious AI-generated art, are all delivered weekly for free to your inbox—sign up now! Barclays' broader research, titled ‘Robots Roll Out, Economies Rewire,’ puts forth that fulfilling the anticipated gap at effective output levels, rather than just nominal employment, would require deploying as many as 24 million humanoid robots across the Chinese workforce by the mid-2030s, representing approximately 4% of the current labor force.

The operational interest of the Barclays note lies in the underlying production dynamics the analysts reference. China has become the hub of the global humanoid-robot supply chain, measured in all available unit shipments.

In 2025, Unitree shipped around 5,500 humanoid robots, leading the global market; Shanghai’s Agibot followed with 5,168 units, while UBTech produced approximately 1,000. The Chinese government has set a target for 2027 for integrating humanoid robots into manufacturing supply chains, along with a goal for a domestic humanoid-robot market valued at 300 billion yuan ($41 billion) by 2035.

Barclays' figure of 'up to 24 million robots' is viewed as a maximum substitution estimate rather than a conservative prediction. MERICS's research on China's embodied-AI strategy provides further context.

The bank's projection anticipates ongoing rapid declines in the costs of humanoid robots (with Unitree's industrial-grade products already retailing below $20,000 in certain configurations), sustained government support for pilot programs between humanoid robot manufacturers and state-owned factories, and the persistence of a 6-8% annual growth in manufacturing wages in eastern China, which has been a key driver for automation.

However, the note takes a more cautious approach regarding the customer side of the supply chain. Independent surveys currently suggest that more than 150 manufacturers operate in the Chinese humanoid market, but only 23% of buyers report satisfaction with their purchased robots.

The operational data provides a reality check, indicating that the deployment of 24 million units to meet Barclays' 60% offset estimate raises questions about commercial readiness that the current evidence does not clearly resolve.

The geopolitical and corporate context adds a third dimension. According to Tesla's own reports, the company is ramping up production of its Optimus robot at its Shanghai Gigafactory, with the third-generation humanoid making its debut at AWE 2026 earlier this year.

Barclays outlines a competitive landscape in which Chinese humanoids not only substitute for human workers in China but also rival Western humanoid offerings (such as Tesla Optimus and Figure 02, 1X Neo) that would otherwise vie for the same factory deployment spaces.

At the industrial scale, the cost differences observed over the past two quarters serve as a key lever.

On a macroeconomic level, Barclays presents a case specific to China. While the labor-force decline and automation parallels are evident in Japan, South Korea, Germany, and much of Eastern Europe, China is unique in combining (a) such a substantial demographic decline, (b) significant domestic manufacturing capabilities for robots, and (c) a policy framework that actively links the two. The note from Barclays articulates how this combination is relevant for macroeconomic forecasts.

What the note does not clarify is the distinction between absorbed and displaced labor. A humanoid robot replacing a worker on a production line is a productivity gain in formal terms. The 60% offset figure presumes that the remainder of the Chinese economy can accommodate the 40% of the labor-force decline not compensated by robots.

The two-decade demographic framework employed by Barclays is broad enough to make this assumption tenable at the macroeconomic level. However, at the level of social policy, this assumption will be a key concern for Beijing’s planning institutions over the next decade.

Other articles

Barclays reports that humanoid robots could compensate for 60% of the 37 million worker shortage in China by the year 2035.

According to Barclays, the use of humanoid robots in China might compensate for up to 60% of the anticipated decline of 37 million workers in the labor force by 2035, necessitating the deployment of as many as 24 million humanoid robots.

Barclays reports that humanoid robots could compensate for 60% of the 37 million worker shortage in China by the year 2035.

According to Barclays, the use of humanoid robots in China might compensate for up to 60% of the anticipated decline of 37 million workers in the labor force by 2035, necessitating the deployment of as many as 24 million humanoid robots.

Nintendo rises 6.8% as Japanese investors shift away from AI.

Nintendo's stock rose by as much as 6.8% on Tuesday, marking the third consecutive day of increases, while Bandai Namco and Konami each saw gains exceeding 9%, as Japanese investors shifted their focus away from AI-related companies.

Nintendo rises 6.8% as Japanese investors shift away from AI.

Nintendo's stock rose by as much as 6.8% on Tuesday, marking the third consecutive day of increases, while Bandai Namco and Konami each saw gains exceeding 9%, as Japanese investors shifted their focus away from AI-related companies.

PlayStation Plus is increasing in price just as everyone is returning.

Sony's recent increase in PS Plus pricing affects monthly and three-month subscribers, just ahead of the anticipated release of GTA 6, which is likely to draw a surge of players back to online multiplayer.

PlayStation Plus is increasing in price just as everyone is returning.

Sony's recent increase in PS Plus pricing affects monthly and three-month subscribers, just ahead of the anticipated release of GTA 6, which is likely to draw a surge of players back to online multiplayer.

Sony no longer aims for “PlayStation exclusive” games to be released on PC.

According to reports, Sony is reducing its PC releases of significant single-player PlayStation titles, indicating a considerable change in strategy following years of growth in the PC market.

Sony no longer aims for “PlayStation exclusive” games to be released on PC.

According to reports, Sony is reducing its PC releases of significant single-player PlayStation titles, indicating a considerable change in strategy following years of growth in the PC market.

The Apple Watch may soon introduce a new feature for sensing blood pressure.

The Apple Watch currently alerts users regarding potential hypertension, but Apple could be developing a more sophisticated blood pressure function for its upcoming premium model.

The Apple Watch may soon introduce a new feature for sensing blood pressure.

The Apple Watch currently alerts users regarding potential hypertension, but Apple could be developing a more sophisticated blood pressure function for its upcoming premium model.

Feldwerke secures a €12 million revolving credit facility to support a 100 MW agri-PV deployment.

The agri-PV developer Feldwerke, located in Munich, has obtained a €12 million revolving credit facility to construct 100 MW of agricultural-photovoltaic capacity within the next 18 months from its 250 MW project pipeline.

Feldwerke secures a €12 million revolving credit facility to support a 100 MW agri-PV deployment.

The agri-PV developer Feldwerke, located in Munich, has obtained a €12 million revolving credit facility to construct 100 MW of agricultural-photovoltaic capacity within the next 18 months from its 250 MW project pipeline.

Barclays reports that humanoid robots could help alleviate 60% of the anticipated 37 million worker shortage in China by 2035.

Barclays states that China's introduction of humanoid robots could compensate for nearly 60% of the anticipated decline of 37 million workers in the labor force by 2035, necessitating the use of up to 24 million humanoid robots.